If you do option trading, then it is very important to know about option Greeks before doing option trading, because there are four factors of option Greeks, which easily explain the change in option. With the help of this, it becomes easy to do option trading and it helps us to buy any option and sell it at the right time.

When there is a change in the index or any stock, there is a change in the calls and puts of that stock or index, which is a very important role of option Greeks.

So let us understand all four factors one by one about Option Greeks.

- DELTA

- GAMMA

- THETA

- VEGA

- RHO

1. DELTA

When there is a change in any stock or index, the price of the option also changes, to which Delta has a very important contribution. Some important things about Delta that you always have to remember.

1. The value of delta for a call option is always 0 to 1, which is positive, cannot be negative than zero, and the value cannot be greater than one, the value of a call option is always positive. Because the price of the option increases when the call option market moves from the bottom to the top.

2. The value of delta for a put option is always -0 to -1, which is always negative and can never be positive. -0 to -1, because the price of the put option increases only when the market moves from top to bottom.

3. The value of the delta for the "At the money" option in any index or stock is always around 0.45 to 0.55. The value of the delta for the "at the money" option is always above 0.50. The delta value for the "Out the money" option is always less than 0.45.

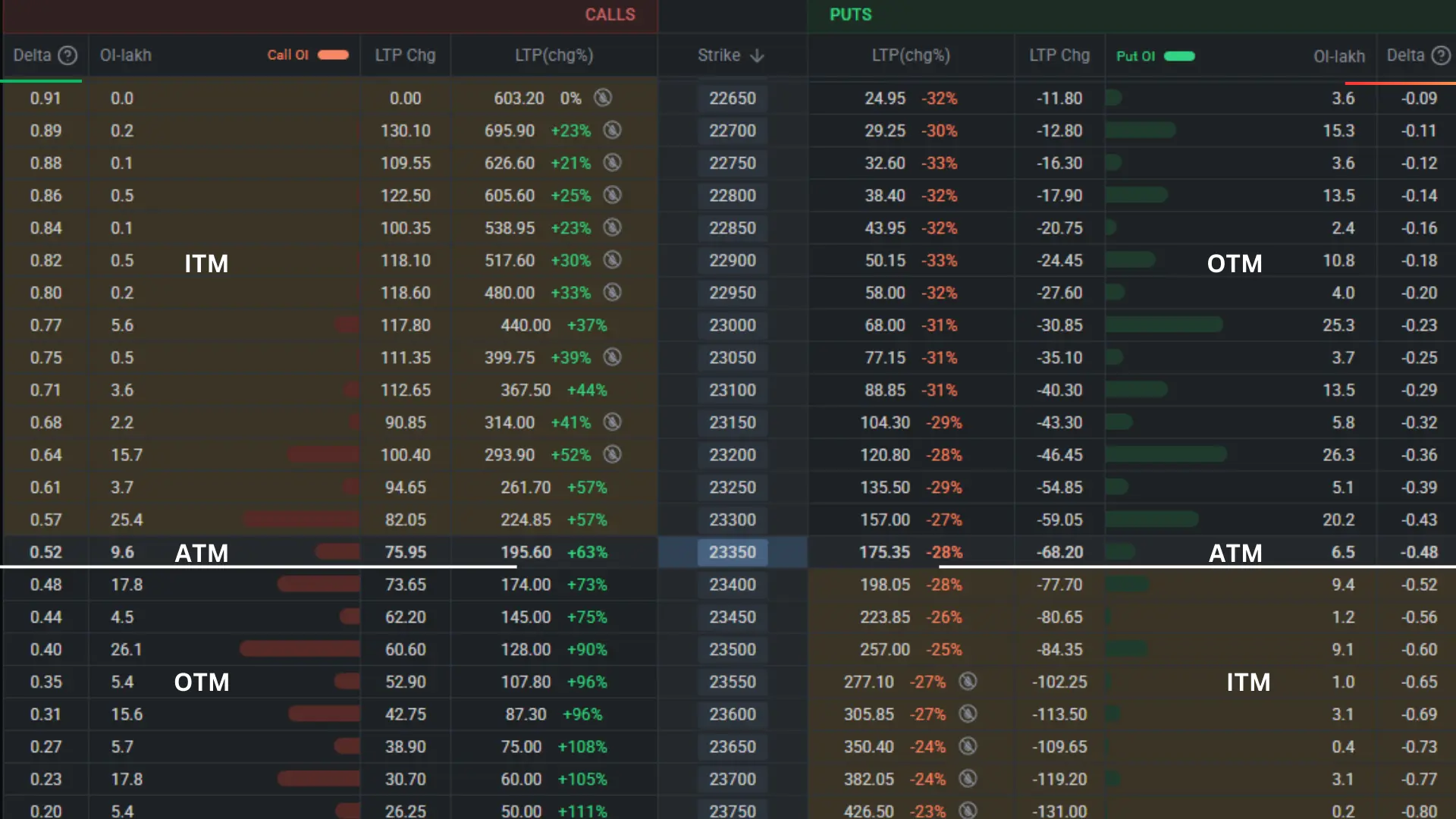

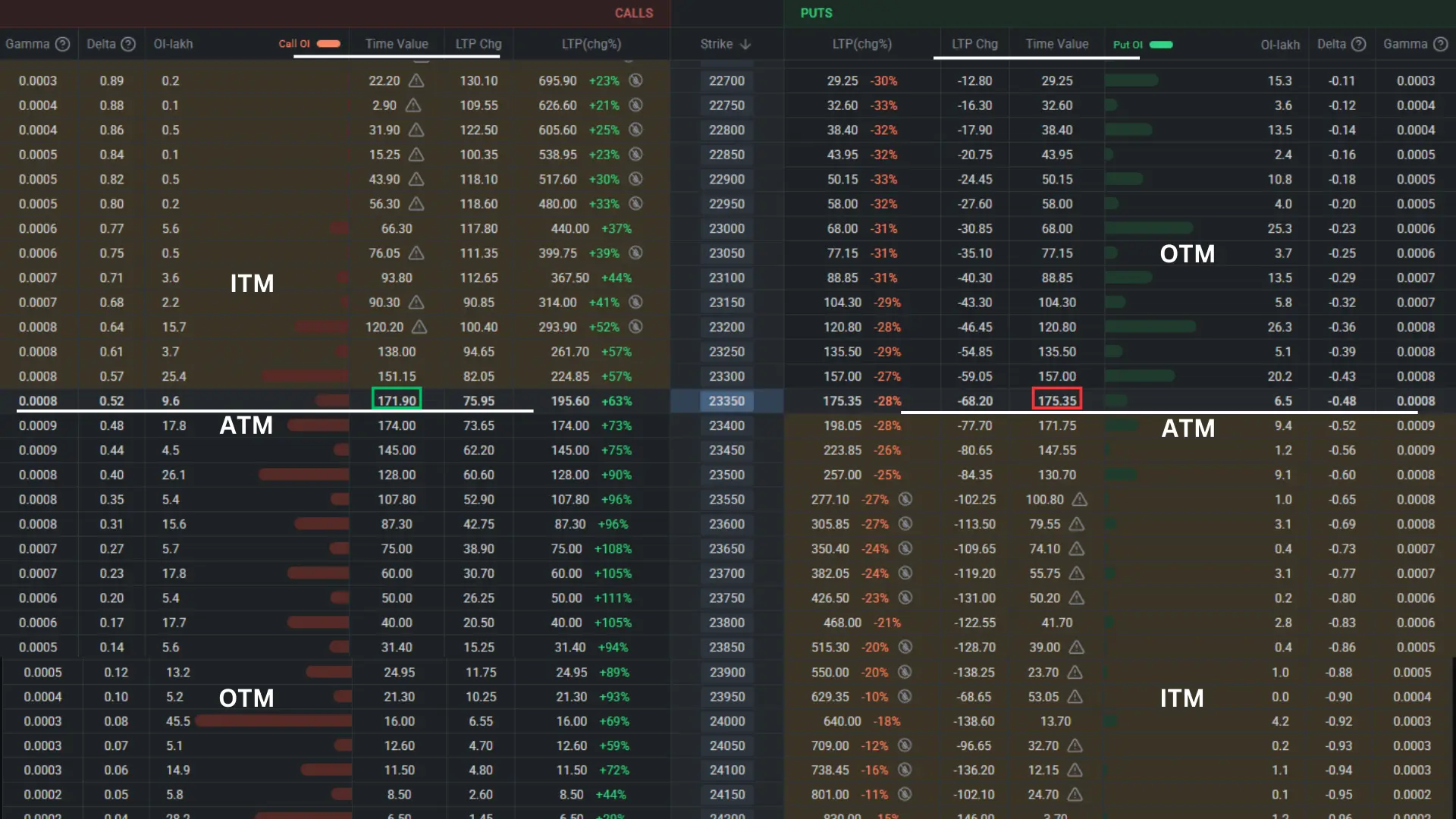

The chart above you can see is taken from Sensibull. There is data from the Nifty index, in which the value of the delta of each strike is given. That is, each strike on the side of the call option has a different delta value. As mentioned above, the value decreases more and more according to In the Money, At the Money, Out the Money, in the same way, the data of the Put option is also shown, in the Put option when the market moves from top to bottom, if it is in decline. Then the price of the put option increases. Whose value is always negative, in this all the strikes have different values according to in the money, at the money, and out of the money strike.

For example, we take a strike and also take the "at the money" Premium price of that strike. Let us calculate how the option price also changes when the index changes.

For an at-the-money call option on the Nifty index 23350, the value of delta is 0.52, so if the Nifty index moves by 1 point, then a change of 0.52 will be the change in the call option of that strike as well. By doing this, if there is a change of 10 points in the Nifty index, in which Nifty reaches 23350 to 23360, then the calculation will be something like this.

MOVEMENT (10) × (0.52) DELTA VALUE = 5.20 Points

Similarly, for put options the delta of Nifty index 23400 put option is negative 0.52, so if there is a 1-point fall in Nifty here, then that 23400 put option will change by 0.52.

While doing this, if there is a fall of 10 points in the Nifty index, then its calculation will be something like this.

MOVEMENT (10) × (-0.52) DELTA VALUE = -5.20 Points

One more thing to be understood here is that, if there is a change of 40 to 50 points in Nifty, then the value of delta will also change. As the Nifty Index 23350 Call option has a delta value of 0.52 and the Nifty Index 23400 put option has a negative -0.52, the value will not remain the same. If Nifty moves up then that Nifty 23350 call option will become "in the money". There the value of delta will increase from 0.52 to 0.65 or so, if Nifty moves higher, it will increase further. Due to this, the value of the delta will go on increasing, and on being deep "in the money", its maximum value will be up to 1, and it will not be more than 1. If Nifty moves by 1 point when the value of Delta is 1, then the Nifty 23350 call option will also move by 1 point, similarly the same method will work for the put option in case of market downtrend.

Therefore, the option buyer should always buy "at the money" or 1st "in the money" Option. The option should either be an in-the-money option. So that when there is a change in the index, there will be more change in its option and we can earn a big profit from it.

Click here for a Demat Account Opening in Zerodha (Investing and mutual fund free, F&O Per order Rs 20)

2. GAMMA

Gamma measures the change in delta, when there is a change in any stock or index, gamma also changes continuously, which also works to measure the change in delta due to that change in the stock or index. Gamma How much the value of delta will change in the premium of the strike of an index can also be ascertained by Gamma.

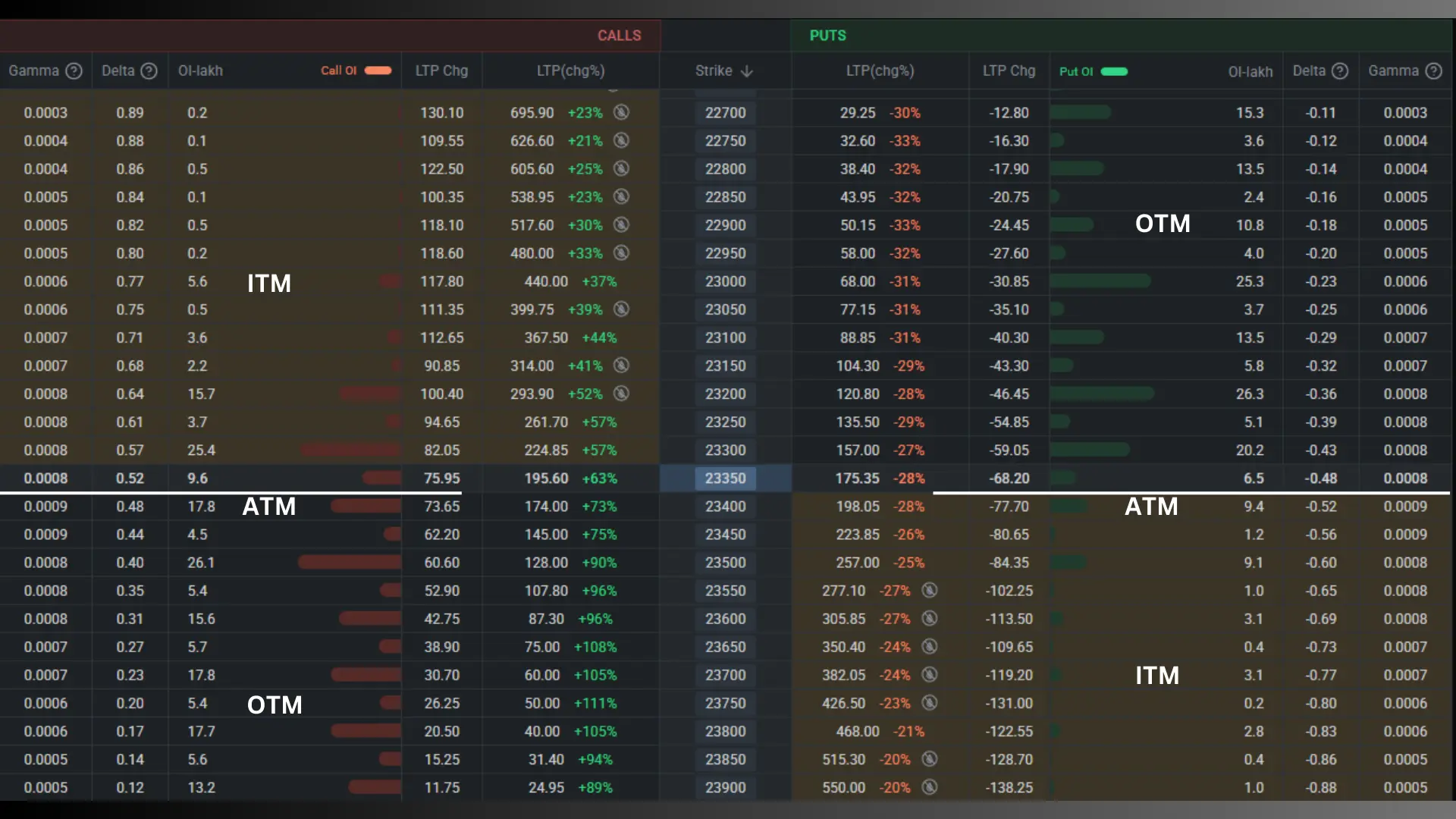

As shown in the below chart for the strike of Nifty, the value of both Call and Put is shown.

From this, we take the example of the call option so that we can do the calculation.

NIFTY 23350CE Price ₹ 195

DELTA value 0.52

GAMMA value 0.0008

And the price of Nifty is 23550, if Nifty moves up by 50 points, then the calculation in theta will be something like this.

NIFTY SPOT PRICE 23350 + 50 (Change) = 23400 (NIFTY NEW SPOT PRICE)

DELTA VALUE (0.52) × (50) NIFTY CHANGE POINTS= 26

NIFTY 23350CE old price 195, after 50 POINT change new price will be 195+26= 221

Calculating Gamma

The value of GAMMA is 0.0008, for a 50-point change in Nifty, the changed point will be multiplied by the value of Gamma.

New gamma value = old gamma value (0.0008) × (50) NIFTY CHANGE POINTS= 0.04

So, for a 50-point change in Nifty, the new Gamma value will be 0.040, which will be used to add the old value of Delta.

So, we can say that before the 50-point change in Nifty, the value of the delta was 0.52, now

That new value of data = old data value (0.52) + New value of gamma after 50-point change (0.04) = 0.56 thus the new value of delta has become.

0.56 is the new delta value, from here on the Nifty will change by 0.56 per point.

So, this way gamma measures the change in delta, where a 50-point change is a 0.056 change in delta.

Click here for a Demat Account Opening in Zerodha (Investing and mutual fund free, F&O Per order Rs 20)

3. THETA

Theta tries to tell us, how much time is left for the option to expire on any stock or index, Theta refers to the time decay (Time decay) of the option. The value of theta is always negative for both the call option and the put option, as the time given to the option expires gradually.

Theta is the enemy of option buyers because the value of theta decreases with time. After buying the option, the buyer of the option can earn profits if the market moves accordingly. If the direction of the market is reversed or if there is no change in the market, then in both cases losses have to be incurred.

Theta is a friend for option sellers, where the value of theta decreases over time, and the seller benefits, even if the index or stock does not change. After selling the option to the option seller, profit can be made if the market moves according to them, but if the value of theta is low, even if the market does not change, profit can be made. Only if the market moves against the position created according to it, there can be a loss.

In the above picture, you can see that the value of 23350CE & 23350PE have 171 and 175 point time decay in option trading.

Before understanding Theta, let us understand some important things so that theta can be understood well.

1. How is the premium for any index or stock option determined?

OPTION PREMIUM = INTRINSIC VALUE + TIME DECAY

The option premium is calculated by adding the Intrinsic Value and the remaining Time decay.

Let us understand it briefly.

The Spot price of NIFTY is 23370 and the value of NIFTY 23350CE is Rs 195 as shown in the chart of Sensibull. Where the strike price of Nifty 23370 where 20-21 points above the spot price of Nifty, then we can say that (23370-23350) 20 points is our Intrinsic Value, and the remaining Rs 170 is Time decay which is mentioned in option chain.

2. Nifty and Bank Nifty options have Weekly and monthly expiry, while Stock options have Monthly expiry. This means the option expires every Thursday in Weekly expiry.

On Friday, the premium price of the option will be higher because there is more time left for the option to expire. As the time frame decreases, the premium value of the option will also decrease if the Nifty does not change much.

If Nifty does not change much on Monday, then the value of Time decay will decrease, due to which the premium price of the option will also decrease. Similarly, in the above example, if the price of Nifty 23350CE is around 23350, if Nifty does not change, then we will get only Intrinsic Value, which will be worth ₹205 only.

Let's take another example of Nifty is trading 23350, where the value of Nifty 23400 CE is ₹ 174, in which Intrinsic Value is 0 or for "at the money" intrinsic value is zero, and ₹174 is full-time decay, so if the number of positive points Nifty closes above 23400 here, its Intrinsic Value will be paid. If it closes below 23400, then the Time decay value will be zero at expiry.

Click here for a Demat Account Opening in Zerodha (Investing and mutual fund free, F&O Per order Rs 20)

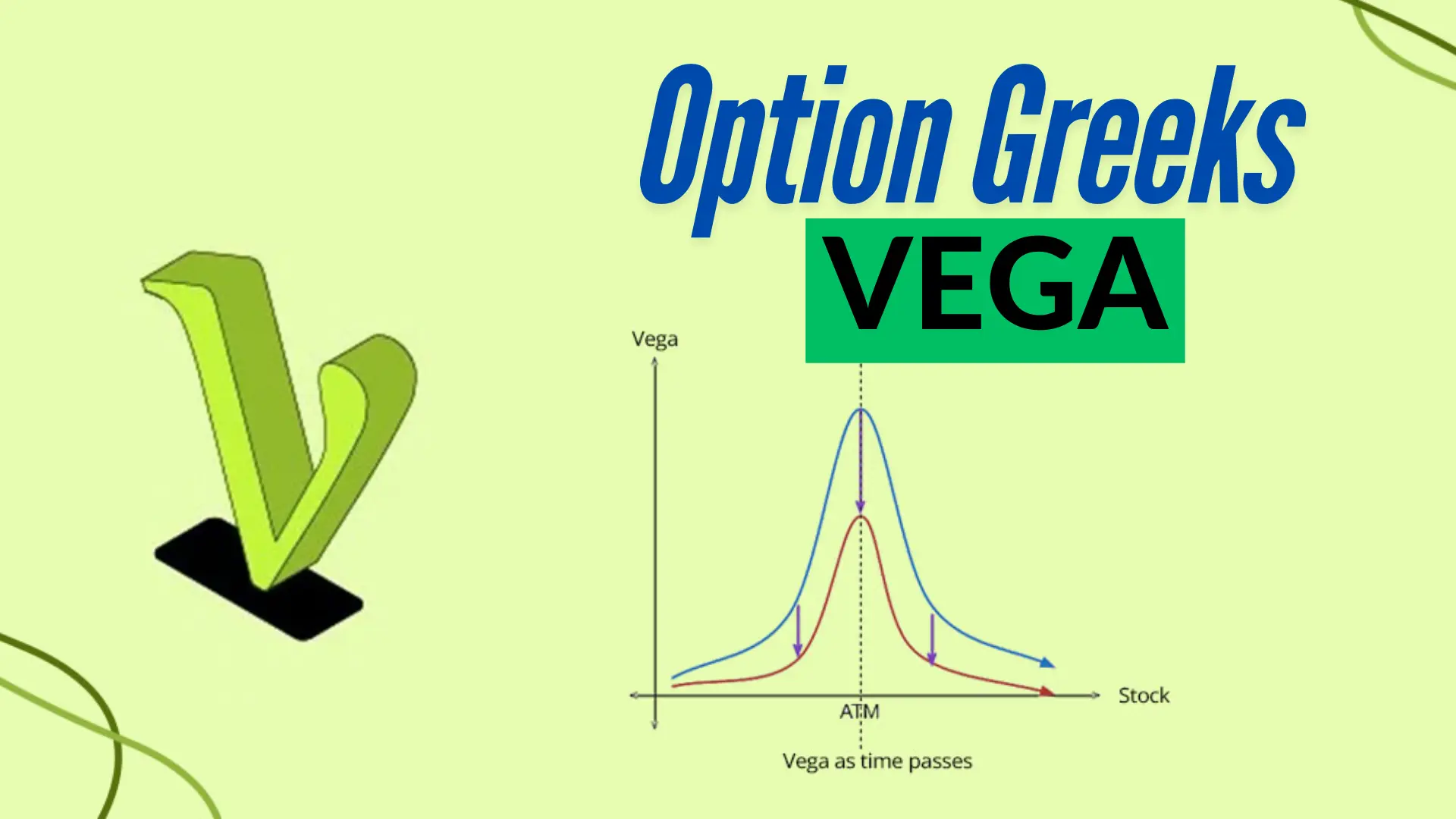

How much does Vega work in the market?

4. VEGA

Volatility based on these, the work of showing the change in the option premium is done by Vega Greek. When the volatility is high in the market, there is a sharp fall or rise in the premium of the option, the increase in the premium of the option Vega indicates a decline. It is worth noting that high, volatility makes the option premium more expensive. Since the strike premium changes very quickly due to volatility, usually when the volatility is low, the option writer makes more profit and vice-versa for the option buyer. Since long options position traders to profit when prices rise, and short options position traders to profit when prices fall, this is why long options have positive Vega while short options have negative Vega.

For example, in the figure shown above, the 23350CE strike is worth 195, Volatility 13.3, and Vega is 6

Now suppose that when volatility 13.30 increases to 15.30, which means 2 points volatility, there is an increase in so now the value of the option will increase to 2 x 6 = ₹12. This means new premium should be = 93.30+12 = ₹105.30

5. Rho

Rho is the part of option Greek that measures how sensitive an option's price is to changes in interest rates. In simpler terms, it tells us how much the price of an option might change if interest rates go up or down.

It's worth noting that rho tends to have a smaller impact on option prices compared to some of the other Greeks, especially for options with shorter expiration dates. Rho can be important, especially for long-term options.

Here's how rho typically behaves:

- For call options, rho is usually positive. This means that as interest rates increase, the value of the call option tends to increase as well.

- For put options, rho is usually negative. So, when interest rates go up, the value of the put option tends to decrease.

Why does this happen? Well, it's related to the concept of the time value of money. When interest rates are higher, the present value of the option's exercise price becomes lower, which is good for call options but not so great for put options.

How to Calculate Rho?

Now, I won't bore you with complex formulas, but it's good to know that rho is typically expressed as the expected change in the option's price for a 1% change in interest rates. For example, if a call option has a rho of 0.05, its price would be expected to increase by ₹0.05 if interest rates increased by 1%.

Click here for a Demat Account Opening in Zerodha (Investing and mutual fund free, F&O Per order Rs 20)

{kind=link}